Table of Links

Table of Links

2. Financial Market Model and Worst-Case Optimization Problem

3. Solution to the Post-Crash Problem

4. Solution to the Pre-Crash Problem

5. A BSDE Characterization of Indifferences Strategies

Acknowledgments and References

Appendix A. Proofs from Section 3

Appendix B. Proofs of BASDE Results from Section 5

Appendix C. Proofs of (CIR) Results from Section 6

4. Solution to the Pre-Crash Problem

It is now left to find the optimal pre-crash strategy π. This is the main concern of the present paper.

Given the known solution to the post-crash problem, we simplify the worst-case problem as follows. First, ignore the constant term log x in the objective. As long as x > 0 its value does not matter for the optimal choice. Second, rewrite the remaining objective as

We arrive at the following problem

Problem 12 (Pre-Crash Problem). Choose a portfolio strategy π ∈ A to maximize

In the following we define the process

Remark 13. The seminal work [49] also defines a crash exposure process, but with respect to wealth, which is different from the exposure w.r.t. utility which we introduce here.

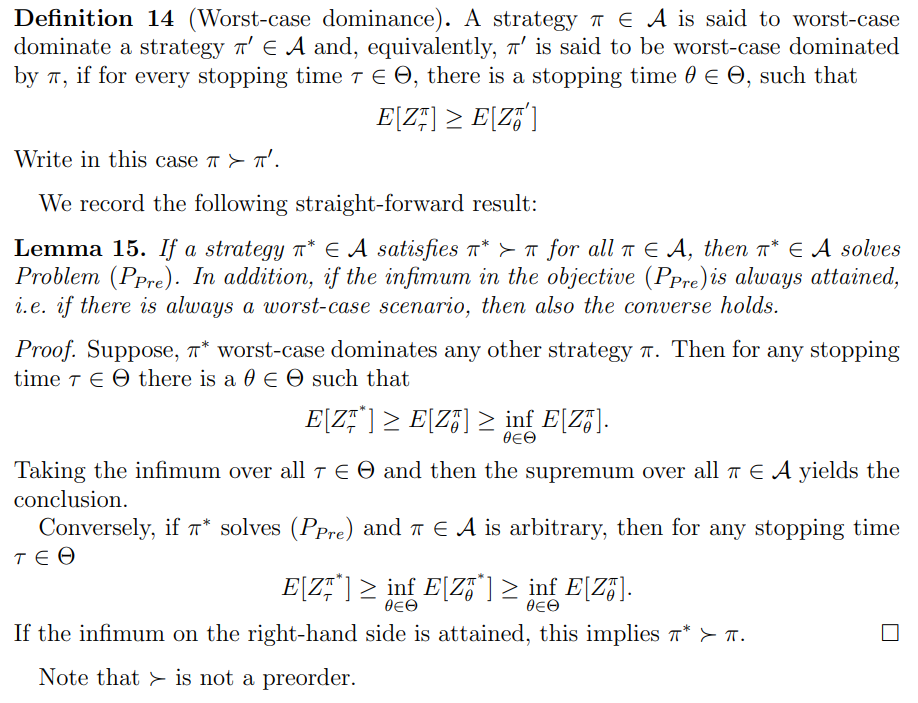

In order to properly characterize (worst-case) optimality of strategies, we introduce the following notion:

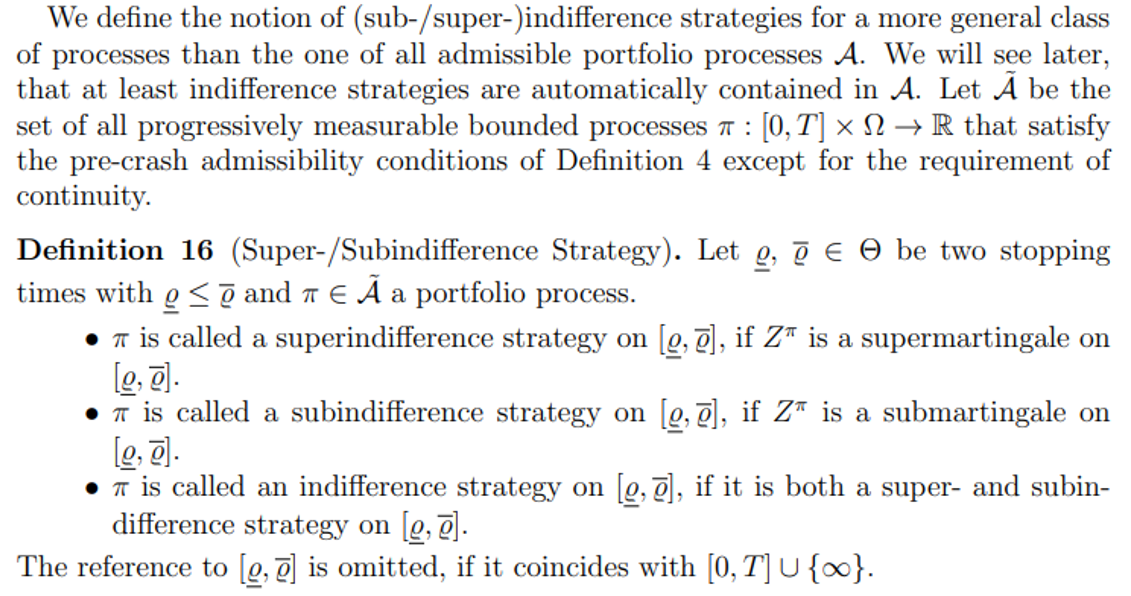

4.1. Super- and Subindifference Strategies. In this section we extend the definition of an indifference strategy to the terms superindifference strategy and subindifference strategy and derive several results to bound the worst-case optimal strategy - if it exists - from below and above.

In the controller-vs-stopper-game setting of [49] we can interpret these strategies as follows:

• A subindifference strategy is a strategy such that at any given time the market/stopper’s best response is to stop the continuation game starting at that time immediately.

• A superindifference strategy is a strategy such that the market/stopper’s best response is to wait forever and never stop the game early.

• An indifference strategy is a strategy such that the market/stopper is at any point in time indifferent between stopping and waiting.

In what follows we also need to be able to concatenate strategies:

We will also make use of the following lemma throughout the remainder of the section.

4.2. The Subindifference Frontier. The following is an enhancement of the classical indifference frontier result of [49] for the log utility case with stochastic market coefficients

4.5. Worst-Case Optimality of Indifference Strategies. Next we prove the crucial optimality result for the worst-case problem with stochastic market coefficients. In particular, this optimality holds whenever the indifference strategy is dominated by the post-crash optimal strategy

Authors:

(1) Sascha Desmettre;

(2) Sebastian Merkel;

(3) Annalena Mickel;

(4) Alexander Steinicke.

This paper is available on arxiv under CC BY 4.0 DEED license.