Table of Links

2. Financial Market Model and Worst-Case Optimization Problem

3. Solution to the Post-Crash Problem

4. Solution to the Pre-Crash Problem

5. A BSDE Characterization of Indifferences Strategies

Acknowledgments and References

Appendix A. Proofs from Section 3

Appendix B. Proofs of BASDE Results from Section 5

Appendix C. Proofs of (CIR) Results from Section 6

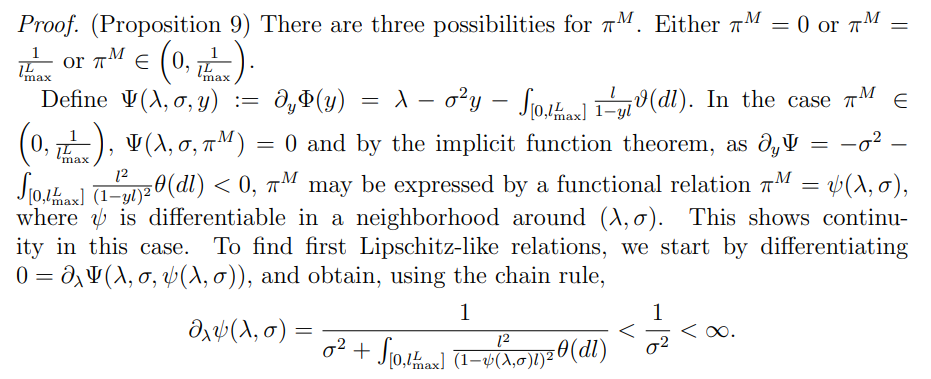

Appendix A. Proofs from Section 3

The same works for the derivative in direction σ,

Authors:

(1) Sascha Desmettre;

(2) Sebastian Merkel;

(3) Annalena Mickel;

(4) Alexander Steinicke.

This paper is available on arxiv under CC BY 4.0 DEED license.